No money for a European clean energy programme? Europe spent nearly the US IRA budget on energy price subsidies and handouts during the 2022 gas crisis.

Following my remarks at BNEF's London Summit (8 October), as requested, here are the numbers and sources for this calculation.

Summary

In 2022 Europe (EU27 plus the UK) found the money for measures to shield citizens and the economy from damaging energy prices and to rescue too-big-to-fail energy companies. In round numbers, this spending choice by (mainly) Germany, Italy, France, and the UK, on what we can label ‘price cushioning subsidies’ plus ‘bailouts’, totalled at least EUR 298 bn. This is the equivalent of 85% of the USD 370 bn provided under the US Inflation Reduction Act for Energy Security and Climate Change investments.

1. Europe’s 2022 gas crisis handouts totalled EUR 255 bn / USD 270 bn

Around 2022, to address energy price differences compared to 2021, the EU27 and the UK spent approximately EUR 255 bn / USD 270 bn on handouts to consumers and companies (December 2022 exchange rate).

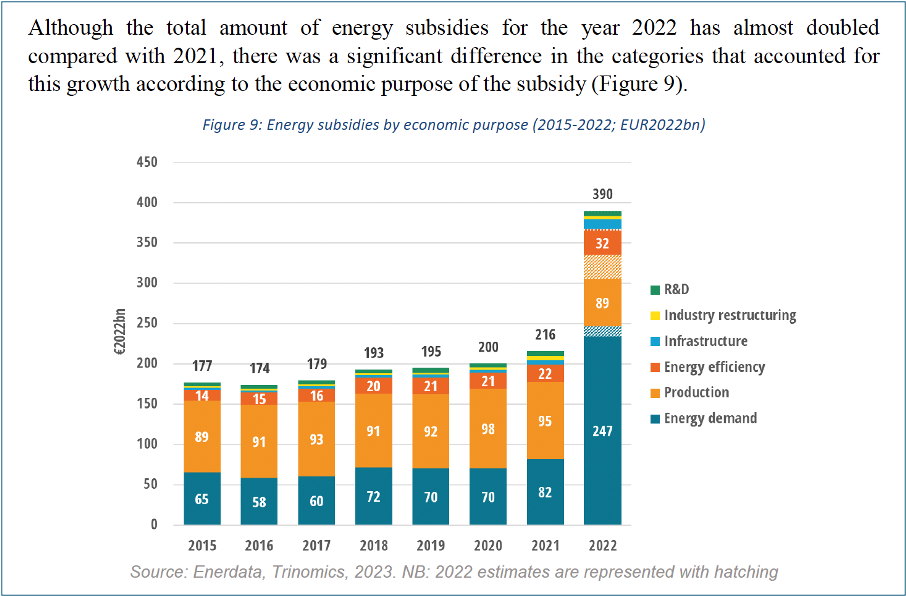

The EU27 data is here: “In 2021-2022, energy subsidies linked to new national measures to protect EU consumers from the high prices accounted for an estimated EUR 195 billion. Across the EU, at least 230 temporary national measures were introduced to address the energy price crisis. Households were the main direct beneficiaries of these support measures (EUR 58 billion), followed by business and industrial consumers (EUR 45 billion) and road transport (EUR 23 billion). Cross-sectoral support was EUR 69 billion.” (EC. October 2023. Report from the Commission to the European Parliament and the Council: 2023 Report on Energy Subsidies in the EU. COM(2023) 651 final).

The Commission concludes that “Subsidies to address the energy crisis measures accounted for 1.12% of the EU’s GDP in 2022. Italy, France, and Germany accounted for almost 70% of this total spending.” As it acknowledges, “Most of the fossil fuel subsidies allocated in the EU-27 since 2015 have been intended to support consumers’ energy demand, for example by limiting the costs of energy consumption through lower tax rates on energy products. The share of these energy demand measures grew from 67% in 2015 to 74% by 2021 and estimates suggest that they will have grown to 83% of fossil fuel subsidies in 2022. Fossil fuel subsidies have aimed at supporting electricity production ranged between 20% and 30% since 2015, and are estimated to have dropped to 10% of all fossil fuel subsidies in 2022.”

The Commission report is drawn from data from an annual external study by Enerdata and Trinomics, 2022 edition. The 2023 edition of this study is also now available.

The report and study use the WTO definition of subsidies as: “government measures falling into one of the following four categories: (i) direct transfers of funds; (ii) government (tax) revenue that is otherwise foregone (not collected); (iii) governments providing goods and services or purchasing goods; and (iv) price and income support.”

The UK data is here: “Initial outturn data shows that the total net cost of energy support policies in 2022-23 was GBP 51.1 bn.” (Office of Budget Responsibility. October 2023. Forecast evaluation report – October 2023: The cost of the Government’s energy support policies).

This included a variety of consumer help schemes over UK financial year 2022-23 (April 2022 to March 2023): the Energy Bills Support Scheme providing a non-repayable GBP 400 energy bills discount to all households, an energy bills cap, a one-off cost-of-living payment to vulnerable households, a GBP 150 rebate on Council Tax, an energy bill relief scheme for businesses, and a cut in fuel taxes. It also included the bailout of Bulb Energy at GBP 2.1 bn. The OBR’s net outturn deducts income from windfall taxes on energy producers via the Energy Profits Levy and the Electricity Generator Levy, which raised a combined GBP 6 billion.

In round numbers, at October 2023 exchange rates, the UK spend was almost EUR 60 bn.

2. Company rescues totalled at least another EUR 43 bn

Additional to the consumer handouts, the EU27 report notes two examples of direct support to companies: Germany’s EUR 34 bn capital injection into Uniper, and France’s EUR 9.4 bn re-nationalisation of EDF. The Commission excludes these sums from its EUR 195 total: “Since the ultimate aim of these measures was to ensure security of supply as well as lower prices to customers or the wholesale market, they were not included in the subsidy database.” The fact that these were chosen as examples suggests that they were not the only cases, and that other EU Member States may also have provided direct support to rescue companies in difficulty.

3. The total cost of consumer handouts and company rescues

Add the UK EUR 60bn to the EU27’s EUR 195 bn and we’re looking at something in the order of EUR 255 bn for consumers. The cost of company rescues across most of Europe is additional to this figure, and was at least EUR 43 bn (Uniper and EDF). Including rescues brings the total to EUR 298 bn / USD 316 bn.

4. What about over-paying to fill gas storage?

EUR 195 billion for EU27 consumers and EUR 43 bn for company rescues might be an under-estimate. It is not clear whether the Commission report includes gas purchases by Germany’s public buyer, The Trading Hub (THE). THE was created in June 2021 to operate a national Virtual Trading Point for gas and to work in coordination with the Federal Network Agency (BNetzA) and the Federal Ministry of Economics and Climate Action (BMWk). In 2022, THE was given the task to purchase in the market using public funds directly provide by the federal government, in order to make sure that the EU target storage level for 1 November 2022 was achieved. THE fulfilled this mission but subsequently sold the gas at loss.

A May 2023 press release quantifies this loss, stating that, in 2022, THE purchased 50 TWh of gas at an average price of 175 EUR/MWh for injection into storage. “Around 12.5 TWh of this gas was already sold in the winter of 2022-23. The average selling price was around 77.50 EUR/MWh. The sale of the remaining gas began at the start of the winter of 2023-24, and the volumes have now been sold in full, with the average selling price for all of the gas at around 48.50 EUR/MWh.”

Making a reasonable (counterfactual) assumption that the storage mandate put gas sellers in a position to over-charge THE, and with reasonable assumptions about how much of the re-sale losses might have been avoided, maybe this part of the 2021-22 energy spend adds another EUR 6 bn. It is impossible to assess the knock-on impact of THE’s buying on the wider European gas market – which in itself increased pressure on energy prices and thus resulted in a greater need to provide subsidies to cushion consumers from high costs.

5. So what?

Long story short, in Europe in 2022 we found the money for measures to shield citizens and the economy from damaging energy prices and to rescue too-big-to-fail energy companies. In round numbers, this spending choice by (mainly) Germany, Italy, France, and the UK, on what we can label ‘price cushioning subsidies’ plus ‘bailouts’, totalled at least EUR 298 bn.

This is the equivalent of 85% of the USD 370 bn provided under the US Inflation Reduction Act for Energy Security and Climate Change investments (Congressional Budget Office estimate).

Obviously, these numbers are not a perfect set (anyone who wants to, please complete the analysis and carry it forward for 2023-24 and share your findings). Obviously, the European energy price crunch created imperatives which were not faced by US decision-makers. My interest, nonetheless, is the big picture point that we don’t lack money in Europe for energy security, we just make choices about our definition of security and therefore our spending priorities. The political economy matters!

6. Comparisons

Obviously, again, it’s not so simple to compare, but allow two broad-brush points.

1) The standout contrast with the US IRA is the Commission data on Europe’s realignment of priorities in 2022 from subsidising industries to subsidising households.

In 2021, EU energy subsidy spending had broadly similar aims to the IRA. The energy industry was “the most subsidised economic sector in 2021, receiving more than half (EUR 111 billion, 51%) of all energy subsidies that year” and the second largest recipient of support was other industry sectors. In 2022, support to households rose by 240% compared to 2021, while “the energy industry received slightly less in subsidies for 2022 (EUR 109 billion) than it did in 2021, and its share of total subsidies dropped from 50% to 28% between 2021 and 2022.”

Meanwhile, in a sector that was once a success story of European industrial support, domestic solar PV manufacturing investments have stalled. In contrast, analysis by Bruegel and Rhodium shows the impact from the IRA tax credits plus Obama and Trump-era trade tariffs on US solar PV manufacturing, which has surged since Q3 of 2022 by a factor of more than eight.

2) Just for orders of magnitude, let’s compare EUR 298 bn to some other globally important budget envelopes.

approximately 1/3rd of the total USD 940 billion estimated to have been spent worldwide on support for consumer energy affordability during the global energy crisis (IEA WEO 2024)

x3.5 the USD 90 bn / EUR 85 bn approximate total of public and private climate finance commitments in 2022 (Carbon Brief)

x2.4 South Africa’s USD 130.5 bn / EUR 123 bn total national government budget in 2022 (Wikipedia)

x5 Pakistan’s USD 64 bn / EUR 60 bn national government budget in 2022 (Wikipedia)

or, finally, almost 1/3rd of India’s USD 923 bn / EUR 871 bn total national government budget in 2022 (Wikipedia)