Deepening connections between energy, trade, manufacturing and climate are the focus of the latest edition of Energy Technology Perspectives (ETP 2024), the IEA’s flagship technology publication. The IEA highlights that: “The new energy economy that is emerging presents major opportunities for countries looking to manufacture clean technologies, their components and related materials.”

As well as the global trend headlines emphasised in the report, a specific China issue jumps out from the data and charts. This isn’t the China dominance point that we’re all familiar with, but a China vulnerability – a potential Achilles Heel.

China’s GDP growth is increasingly dependent on clean energy technology exports, and therefore dependent on how much competition China faces from other cleantech manufacturers, including the US.

Will Trump’s dislike of clean energy cause the US miss out on a geopolitical and national security opportunity?

1. IEA insights on cleantech trade

In its online summary of the ETP 2024 report, the IEA writes:

“Clean technology supply chains are highly dependent on trade, and will continue to be in the future. At around USD 200 billion, the value of trade in clean technologies is nearly 30% of their global market value. The biggest element is trade in electric cars – which has doubled since 2020, reaching around one-fifth of trade in all cars in 2023 in value terms – while solar PV is in second place. Under today’s policy settings, overall clean technology trade is on track to reach USD 575 billion by 2035, around 50% more than the current value of global trade in natural gas.”

“Despite the ongoing implementation of industrial strategies in other countries, the value of China’s clean technology exports is set to exceed USD 340 billion in 2035, based on today’s policy settings. This is roughly equivalent to the projected oil export revenue of both Saudi Arabia and the United Arab Emirates combined in 2024.”

“China is currently the cheapest location for manufacturing the key clean energy technologies considered in this report, without taking into account explicit financial support from governments. It costs up to 40% more on average to produce solar PV modules, wind turbines and battery technologies in the United States, up to 45% more in the European Union, and up to 25% more in India.”

In the full report, the IEA writes:

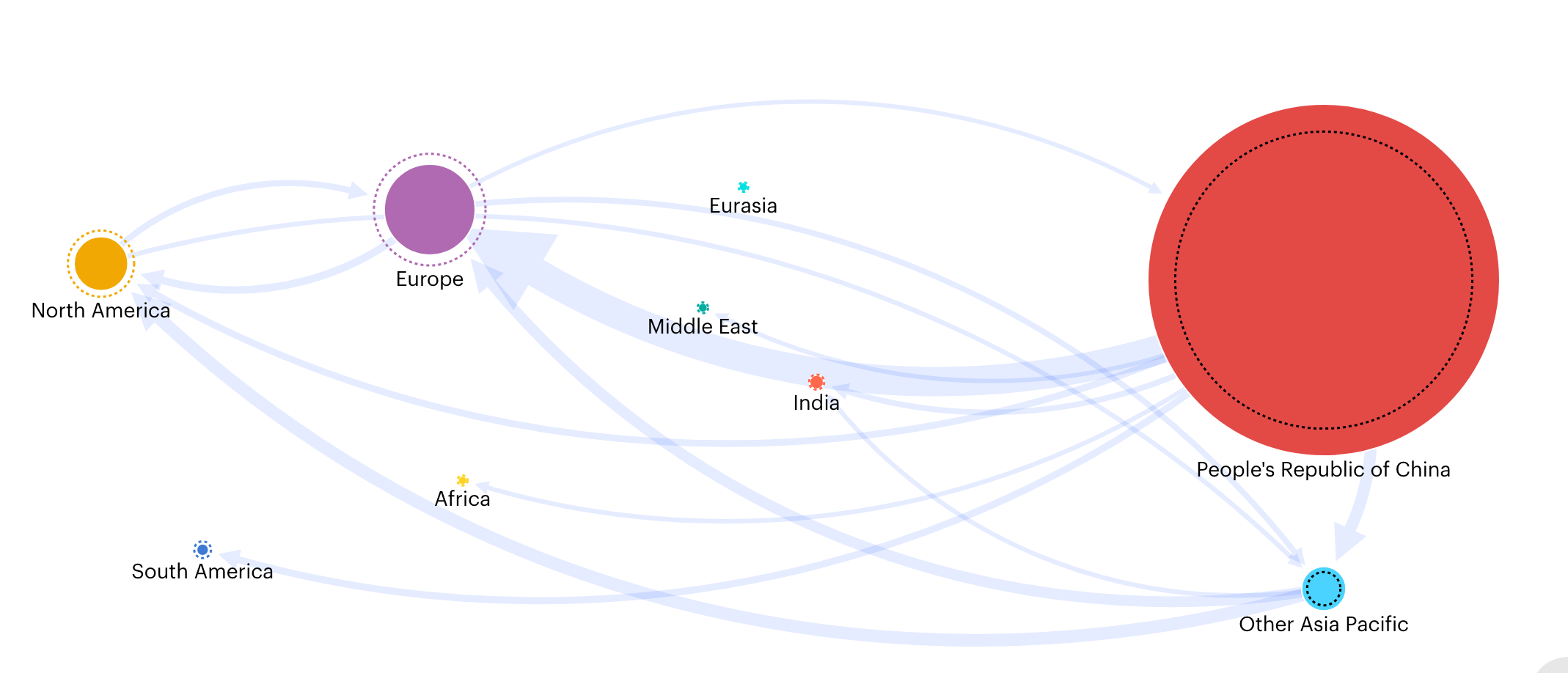

“China is by far the world’s largest exporter of clean energy technologies. China’s exports of clean technologies and materials have grown significantly over the last decade, supported by ample manufacturing capacity, low-cost production, demand growth outside China and favourable policies (Figure 1.19). In 2023, China’s share of global exports of EVs (in units) was over 30%, 65% for solar PV, and 15% for aluminium. China’s installed manufacturing capacity has increased rapidly, with capacity potentially available for exports (i.e. once domestic demand has been met) amounting to 650 GW for solar PV and 7 million electric cars, or 70% and 45%, respectively, of total manufacturing capacity in the country in 2023.”

“The growth of the Chinese economy has begun to slow in recent years as its economy matures and population growth stagnates. In all our scenarios, […] manufacturing shifts towards higher value added sectors, including the “new three” clean technologies (EVs, batteries and solar PV), other electronics, machinery and transport equipment.”

Not exactly spelt out in this series of statements, but loud and clear between-the-lines and joining-the-dots, is a message that clean energy technology exports play a vital role in China’s GDP growth. And therefore, whether (or not) China faces serious competition in global clean energy technology markets is becoming a key strategic factor for Chinese growth – and thus for the country’s risk of economic slowdown.

Certainly, China’s clean energy investment strategy is impacting other countries. But there are two sides to the coin: other countries’ (lack of) clean energy innovation, manufacturing, and trade strategies also matter to China.

2. Role of clean energy technology exports in Chinese GDP growth

According to the IEA, in 2023, China's GDP growth rate was 5.2%. This is on the low end of what China needs to remain stable. Clean energy accounted for about one-fifth of that total growth. But China’s domestic markets for clean energy are saturated, so this growth crucially relies on exports.

Take the example of batteries:

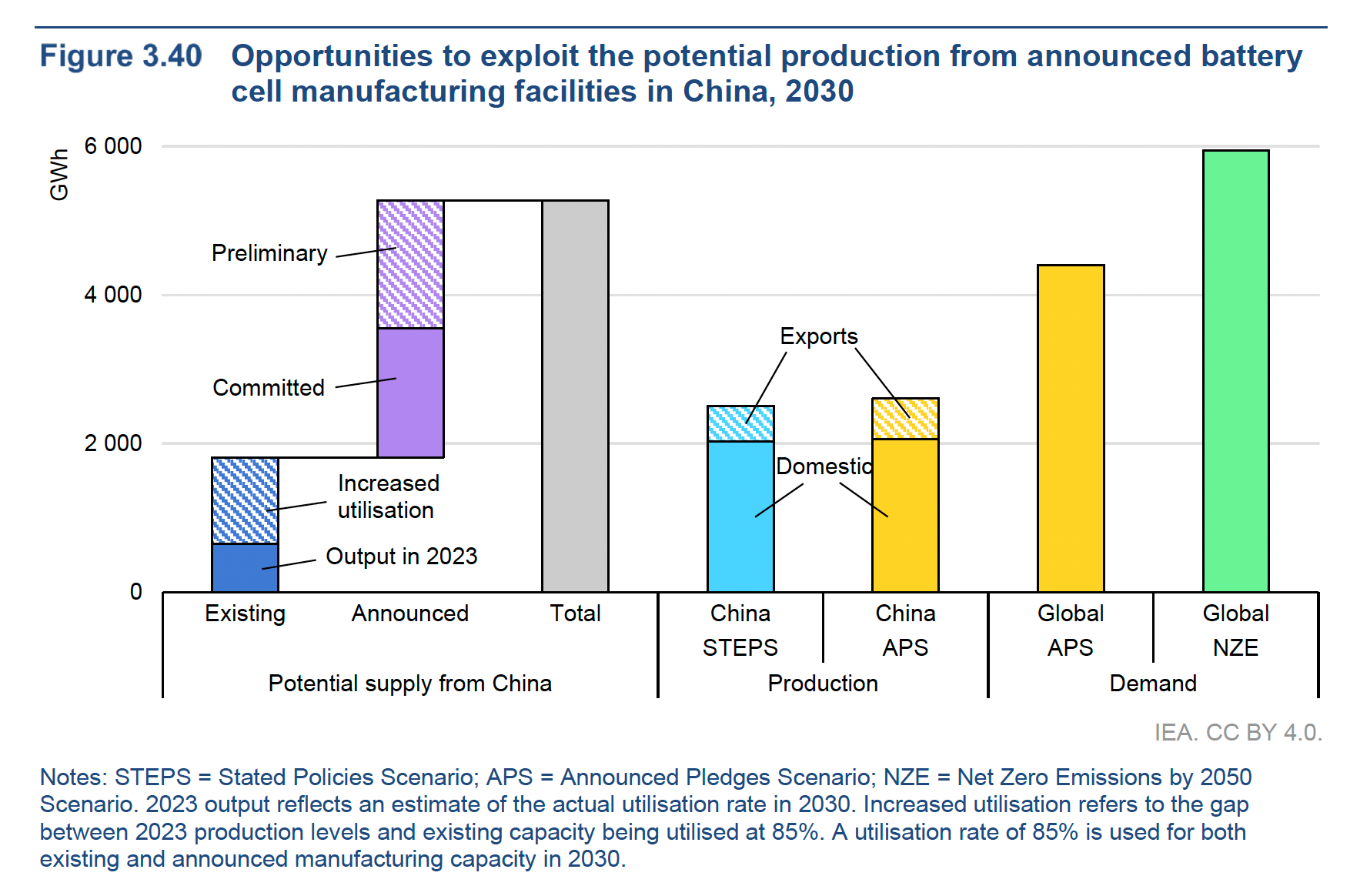

“It is unlikely that domestic demand and export would be sufficient to absorb all of the planned increase in China’s battery cell manufacturing capacity, including all preliminary projects, before 2030. The plants in operation today could already meet 90% of domestic battery demand in the STEPS in 2030 if their average utilisation rate was increased to 85%, from just over 30% today (Figure 3.40). Taking announced capacity expansions into account, total capacity in 2030 would be capable of supplying all of the world’s battery demand in the APS, but 40% of this demand is supplied by other countries in that scenario, thanks to their investments in manufacturing capacity, supported by industrial and trade policies. If climate ambition were to be raised further, and the level of global demand in the APS (4.4 TWh) grew to that in the Net Zero Emissions by 2050 Scenario (NZE Scenario) – reaching almost 6 TWh – it would be equivalent to utilising a further 25% of the existing and announced capacity in China.”

In short, again: China's clean-technology investment boom has helped the country become a leader in clean-energy supply chains. But it has also left Chinese GDP growth highly exposed to export markets, and therefore to competition from other cleantech manufacturers.

3. Will Trump’s dislike of clean energy cause the US to miss out on a geopolitical opportunity?

As the IEA notes, “there are still strong opportunities for countries all over the world to enjoy the benefits of increased clean energy manufacturing and trade, depending on the pace of clean energy deployment and the policies adopted.” Importantly, “The door of the new energy economy is still open to emerging markets.”

By definition, such opportunities are also available to the EU – if it gets its act together. And they are open to the US – if the Trump Administration doesn’t turn its back on investments in cleantech and the energy transition.

In short: the ETP 2024 begs the question whether the Trump team can see the geopolitical and national security dimension of energy transition.

Section 3.3. of the ETP summarises:

“China’s economic development model has relied to a significant degree on export-oriented manufacturing.”

“The prospects for China’s export-oriented clean energy technology industries hinge to a large degree on policies in China as well as the rest of the world to encourage both the deployment of those technologies and the development of domestic manufacturing capabilities. In general, those countries that are heavily dependent on imports are already taking action to reduce reliance on China and other foreign suppliers by stimulating domestic investment with the aim of enhancing energy security and stimulating economic activity.”

“The strength and impact of those policies – covering the broad spectrum of energy, climate and economic development – on the demand for Chinese technologies in the medium term differs markedly between the STEPS and APS, and across technologies. In the former scenario, China’s exports continue to play a central role in meeting the needs of the rest of the world, underpinned by low production costs thanks to large economies of scale and a high degree of supply chain integration. The APS paints a more mixed picture, with faster growth in global demand leading to increases in China’s exports for certain technologies, but for others, the impact of other countries’ policies to develop their own manufacturing capacities is to reduce the need for Chinese exports relative to the STEPS, particularly after 2030.”

(Just to remind: The Stated Policies Scenario (STEPS) reflects the current policy landscape. The Announced Pledges Scenario (APS), explores the impact of additional announced ambitions and targets including both 2030 targets and longer-term net zero or carbon neutrality pledges, regardless of whether these announcements have been anchored in legislation or in updated Nationally Determined Contributions.)

“If China’s GDP is to continue growing at 4–5 percent for the next decade, either other major economies must be willing to reduce their economies’ investment and manufacturing shares to accommodate China or China must establish policies that cause the locus of growth to shift from investment to domestic consumption. Neither is easy, and the former is very unlikely.”